May 2026 opened with cautious optimism, Bitcoin broke through the key $79,500 prior high and briefly touched $82,800 on the back of six consecutive weeks of ETF inflows, easing US-Iran tensions, and robust US earnings. That recovery thesis was abruptly challenged in the second half of the month, when hotter-than-expected inflation data (CPI 3.8%; PPI 6.0%), rapidly rising long-term Treasury yields, and escalating geopolitical risk drove the largest weekly ETF outflow of 2026 and pushed Bitcoin back below its true market cost basis near $78,200.

By month-end, BTC was trading near $72,000–$73,000, down roughly 10–12% from its May peak, with total crypto market cap falling from a high of ~$2.70T to ~$2.45T. The dominant narrative shifted from “recovery breakout” to “sideways consolidation in search of a new direction.”

This May 2026 Crypto Market Report is synthesized from KuCoin’s official weekly reports and enriched with Finestel’s proprietary AUM-weighted institutional tracking data. It combines on-chain metrics, ETF flows, and macro analysis with real-time observations of how professional asset managers actually positioned themselves throughout the month.

BTC Phases in May: From Hope to Reality

Early May (Apr 27 – May 10): The Recovery Thesis Holds

Mid-May (May 11 – May 17): The Macro Shock

Late May (May 18 – May 24): Consolidation Under Pressure

Final Week (May 25 – May 31): The Month-End Flush

Capital Flows: Bitcoin Spot ETF Weekly Net Flows

A critical insight from the flow data: ETF redemptions tracked US Treasury yield movements more precisely than geopolitical news events. When 10-year yields eased mid-week on May 20, daily outflows moderated in real-time, confirming that institutional Bitcoin allocations have become a direct rate-sensitive proxy. The May 13 single-day outflow of $630M coincided exactly with the CPI miss; the May 28 outflow of $733M (IBIT’s second-largest ever daily outflow) coincided with US military strikes on Iranian positions.

Crypto Market Report May 2026: Key Macro Events & Market Impact

| DATE | EVENT | READING / OUTCOME | CRYPTO IMPACT |

|---|---|---|---|

| Apr 29 | FOMC Decision | Hold; statement language turns hawkish | Neutral/cautious |

| Apr 29 | Fed Chair Nomination | Kevin Warsh confirmed 13–11 | Policy uncertainty premium |

| May 1 | Iran Peace Proposal | 14-point plan via Pakistan | +$629M single-day ETF inflow |

| May 5 | AMD Q1 Earnings | Revenue +38% YoY; data center +57% | Risk-on sentiment lift |

| May 8 | US Non-Farm Payrolls | +115K vs. 62K expected | Fed focus shifts to inflation |

| May 12 | US CPI (April) | 3.8% vs. 3.7% exp; core 2.8% | $630M single-day ETF outflow |

| May 13 | US PPI (April) | 6.0% — highest since Dec 2022 | Rate hike prob. rises to 40% |

| May 15 | Powell Steps Down | Warsh sworn in; no cuts before Sep 2027 | Structural hawkish repricing |

| May 19 | 30Y Treasury Yield | 5.18% — highest since 2007 | Broad institutional de-risking |

| May 20 | FOMC Minutes | Many members want to remove easing bias | Hike narrative reinforced |

| May 24 | Trump on US-Iran | “Basically reached an agreement” | Brief relief bounce toward $77K |

| May 28 | US Military Strikes | Strikes on Iranian drone sites near Hormuz | $733M single-day ETF outflow |

Notable Movers: Crypto Market Report May 2026

Capital rotation followed a clear three-act pattern through the month. Early May saw genuine fundamental-driven gains in RWA and Telegram ecosystem tokens. Mid-month brought a speculative BSC small-cap wave driven by leverage and low liquidity rather than fundamentals. Late May saw a flight to quality assets with real revenues, buybacks, or upgrade catalysts (HYPE, NEAR, RAIL) outperformed while the BSC names reversed sharply.

| TOKEN | SECTOR | PEAK WOW | CORE CATALYST | DRIVER TYPE |

|---|---|---|---|---|

| Toncoin (TON) | Ecosystem | +67.9% | Telegram replaces TON Foundation; fees cut 6×; largest validator | Fundamental |

| Ondo (ONDO) | RWA | +48.6% | DTCC working group selection alongside BlackRock, Goldman, JPMorgan; tokenized T-bond exchange | Fundamental |

| Jupiter (JUP) | DEX/RWA | +42.2% | Securitize × Jump Trading on-chain stock trading on Solana; whale accumulation | Fundamental |

| NEAR Protocol | AI Infra | +57.3% | AI proxy infra positioning; dynamic resharding launch; post-quantum signatures in June | Fundamental |

| Hyperliquid (HYPE) | Perp DEX | +36.3% | 97% fee buyback ($214M Q1 income); a16z accumulation; break to ATH above $63 | Fundamental |

| Railgun (RAIL) | Privacy | +201.4% | Privacy narrative revival; Grayscale ZEC buying; TVL ~$120M; low float (57M circulating) | Narrative + Thin Float |

| LAB | BSC | +227.4% | Suspected insider: buy ~$0.2, dump ~$2.3; $26.6M shorts liquidated | Manipulation |

| Ondo / JUP / ICP | Various | –24% to –25% | Profit-taking reversal in week of May 11–17; macro risk-off | Reversal |

Crypto Market Report May 2026: On-Chain Structure

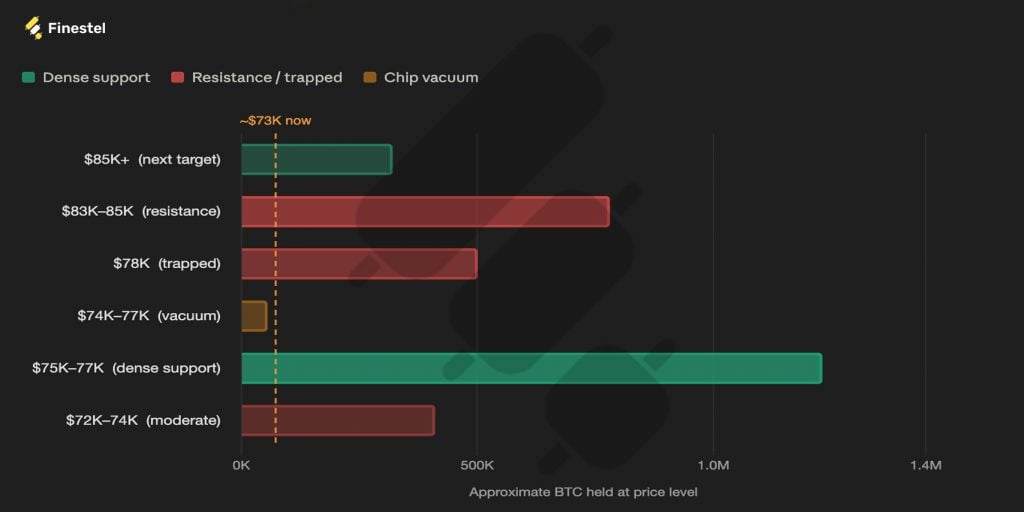

A consistent and reassuring signal throughout May: long-term holders (LTH) showed zero signs of capitulation. All chip movement was confined to the $66K–$78K range, dominated entirely by short-term holder turnover.

The sell-off was not a panic-driven exodus but a systematic institutional de-risking tied to rate expectations, preserving the supply-side foundation for a future recovery. The $76.3K–$77K band, backed by 1.23M BTC in chip density and resonating with EMA60/90, remains the definitive medium-term bull defense line heading into June.

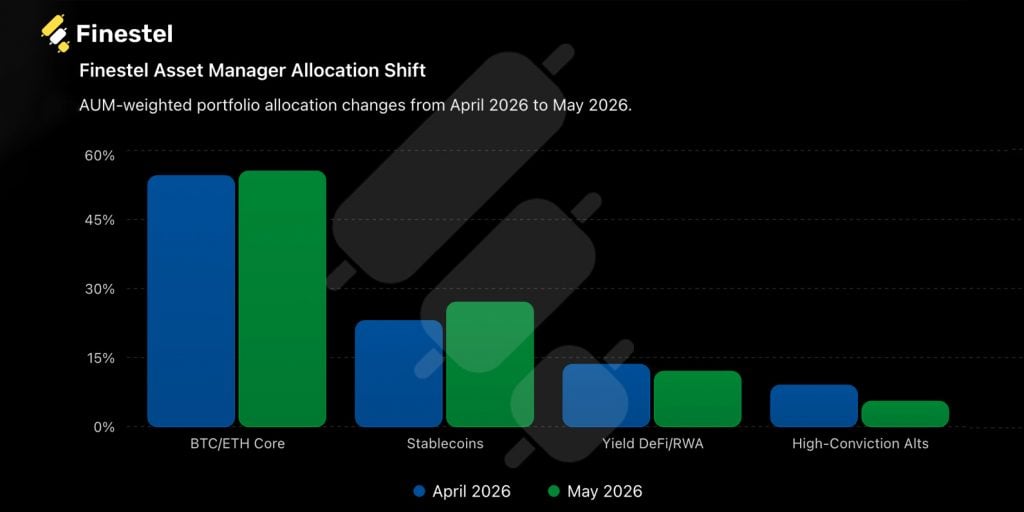

Finestel Insider: The Defensive Re-Allocation

While retail investors and ETF flows reacted emotionally to the macro shocks, Finestel’s proprietary AUM-weighted tracking of professional asset managers told a different story.

Our data shows a clear defensive rotation that accelerated in mid-May as hotter-than-expected inflation data hit the market and Treasury yields spiked. Managers used the early-month strength to raise liquidity and reduce high-beta exposure, while modestly reinforcing core positions on weakness.

This was not a reactive scramble, but a disciplined execution of risk management.

May 2026 Allocation Shift (AUM-Weighted)

| Allocation Category | April 2026 | May 2026 (End) | Net Change | Strategic Commentary |

|---|---|---|---|---|

| BTC/ETH Core | 54.5% | 55.5% | ▲ +1.0% | Flight to quality. Managers added on dips, treating BTC as the ultimate macro hedge. |

| Stablecoins | 23.0% | 27.0% | ▲ +4.0% | Significant liquidity raise. Dry powder increased to defend against volatility and prepare for better entries. |

| Yield-bearing DeFi / RWA | 13.5% | 12.0% | ▼ -1.5% | Reduced exposure to volatile yield strategies in favor of capital preservation. |

| High-Conviction Alts | 9.0% | 5.5% | ▼ -3.5% | Beta purge. Exposure cut sharply as risk appetite cooled. |

| Leverage Ratio | 1.1–1.2x | 1.0–1.1x | ▼ De-risk | Leverage was kept minimal. Focus shifted to spot + options hedging. |

| Portfolio VaR | ~7.0% | ~6.5% | ▼ Tighten | Improved risk control despite elevated market volatility. |

- The rotation began around May 12–15, coinciding with the hotter CPI print. Managers systematically distributed into strength and raised stablecoin reserves, a textbook defensive move.

- Core BTC/ETH exposure was protected aggressively. Many managers viewed the asset as the “only safe house in a bad neighborhood” during the macro storm.

- High-conviction altcoin exposure was culled to the strongest AI infrastructure, privacy, and Layer-1/2 names only.

- Overall portfolio risk (VaR) was actively lowered even as the broader market became more volatile.

This disciplined approach once again highlights the gap between professional asset managers and the broader market. While ETF investors were net sellers in the second half of May, Finestel-tracked managers were quietly repositioning for the next leg, whatever direction macro conditions ultimately dictate.

Crypto Market Report May 2026: Regulation and Compliance

May was a consequential month for crypto regulation globally, with the US leading a flurry of legislative activity. The clearest signal of the longer-term regulatory direction: both the CLARITY Act (digital asset market structure) and the NYSE tokenized securities framework took meaningful steps forward, indicating that institutional infrastructure for on-chain finance is being actively built at the policy level.

CLARITY Act Advances

Bitcoin Reserve Act; Revised

SEC & NYSE Tokenized Securities

Pro-Crypto State Bills

South Korea Tax & Japan ETF

MiCA Adoption & Russian Tightening

Outlook: Market Structure Entering June 2026

↑ Bull Case

The $76.3K–$77K support zone, backed by 1.23M BTC in on-chain chip density and resonance with EMA60/90, holds. A US-Iran deal materially reduces the geopolitical risk premium. Treasury yields stabilize or retrace from extreme levels. ETF inflows resume, anchored by institutional reallocation. If BTC can reclaim $78K and then clear the $83K–$85K resistance band, the path to a genuine trend reversal reopens.

↓ Bear Case

The $76.3K defense breaks decisively. A chip vacuum between $72K and $77K means the next natural equilibrium is near $70K with little structural support in between. Continued ETF redemptions, inflation persistently above expectations, further Treasury yield rises, or US-Iran military escalation each represent credible triggers. The month-end price (~$73K) had already encroached on this vacuum zone.

The overarching theme entering June is macro dominance. Bitcoin has not yet established an independent narrative capable of decoupling from rate expectations, a stark contrast to the RWA-driven altcoin strength and the genuine on-chain progress seen in tokenization, stablecoins, and DeFi revenue models. Three structural pressures, tightening monetary policy, geopolitical risk, and technical overhead resistance, must ease simultaneously before a sustained uptrend resumes. The one reassuring signal is long-term holder conviction: zero LTH chip loosening throughout the month confirms that the sell-off was institutional de-risking, not capitulation. That foundation remains intact, waiting for the macro backdrop to turn.

Leave a Reply